Who are the super app contenders in Europe?; Successful implementation of hyper-personalization in banking; What makes super apps super?;

In this edition:

1️⃣ Who are the super app contenders in Europe?

2️⃣ Who distributes embedded finance, and what products do they offer?

3️⃣ N26 has today launched cryptocurrency trading

4️⃣ Fintech giant Plaid is releasing its first crypto-native product called “Wallet Onboard”

5️⃣ IoT payments will help accelerate the development of sharing economy platforms

6️⃣ Wallets are exploring several monetization paths

7️⃣ What makes super apps super?

8️⃣ Successful implementation of hyper-personalization in banking

9️⃣ India Fintech Report 2022: Sailing Through Turbulent Tides

🔟 20 open banking use cases you should know about according to Yapily

***

Who are the super app contenders in Europe?

Asia has the likes of WeChat, Alipay, Grab and Gojek. But will Europe ever get a superapp of its own?

Who are the contenders in Europe?

So far, four European startups have made their superapp intentions clear: Klarna, Revolut, Bolt and Lydia.

Klarna

Klarna hasn’t ever publicly said it’s vying for superapp status, but all its acquisitions and product rollouts point to something like that. When Klarna acquired comparison site PriceRunner last November, it made its ambition to take on Amazon, Google and Meta clear. It offers banking services like current accounts and savings only in its most mature markets, Sweden and Germany — but it wants to roll them out globally. Its customer base is substantial, but it faces a huge challenge trying to get its buy now, pay later customers to switch from their legacy banking providers or neobanks to a current account with Klarna.

Lydia

When fintech Lydia raised a $133m Series B last December, cofounder and CEO Cyril Chiche told Sifted that the company was now racing Revolut for financial superapp status. “The superapp is really the future of banking services as we know them,” he said. Lydia recently launched crypto trading and savings functions, and is plotting new credit and investment products. But it’s only really taken off in France, and has a fraction of the customer numbers of the other three contenders. It’s still predominantly focused on payments, and the market entries it’s plotting — Portugal and Spain — are already served by larger rivals like Revolut.

Bolt

Estonian Uber-rival Bolt describes itself as “Europe’s leading mobility platform and first superapp”. It’s raised big cash in quick succession for its plans to expand its offering in ride-hailing, scooter rental, car sharing and food and grocery delivery. Andrew Reed, partner at Sequoia, one of the company’s big-name investors, tells Sifted that this multi-product offering is all part of its goal to reduce the need for private car ownership in urban areas. “Offering just one of these solutions is not enough to enable such a broad mission,” Reed says. But its food and grocery delivery plans are still in their infancy — and will prove tricky to win customers from more established rivals like Uber Eats, Deliveroo, Gorillas and Getir.

Revolut

Most investors agree that the closest thing Europe has to a super app so far is Revolut. The fintech openly refers to itself as a “financial super app”, and has launched 54 products, ranging from debit cards and bank accounts to crypto trading, holiday insurance and even business banking. And as of last week, it’s branched into commerce with the launch of shopping app Revolut Shops in Ireland.

Unlike it neobanking peers Monzo and N26, Revolut has pursued a multi-product strategy from the outset that included international money transfers years before its competitors. This one-stop convenience has led to its customer base being at least double either rival.

Source Sifted

***

Who distributes embedded finance, and what products do they offer?

Embedded finance is likely to emerge in any environment in which a critical mass of end customers (consumers or businesses) have frequent (often daily) digital interactions with the operator of the digital platform, which we refer to as the “distributor” of embedded finance. For a nonbank company acting as a distributor, embedded finance offers a way to enhance the customer experience and create a new source of revenue without incurring the overhead associated with operating a bank. The types of businesses well placed to offer embedded finance include retailers, business software firms, online marketplaces, platforms, telecom companies, and original equipment manufacturers (OEMs). All these categories have seen high levels of activity and innovation in embedded finance during the past year or two.

Among embedded-finance distributors and their end customers, demand is already maturing for a range of deposit, payment, issuing, and lending products. In addition to these traditional financial products, novel use cases are emerging. For example, embedded-finance distributors are offering prepaid cards to employees as part of earned-wage access programs; giving merchants the option to use their deposit accounts for instant payments settlement. Some are providing just-in-time funded debit cards for gig economy workers to use when making purchases for members of delivery-service platforms.

The embedded-finance product portfolio is likely to expand further as customer-onboarding and product-servicing processes are gradually digitized and real-time risk analytics and services grow more sophisticated. Risk is likely to remain a constraint on growth, however, as products that require case-by-case assessment, in-person touchpoints, or regulatory waiting periods, such as commercial real estate financing, are less susceptible to end-to-end digitization. Despite these constraints, we estimate that products suitable for offering via embedded finance could account for as much as 50 percent of banking revenue pools.

Source McKinsey & Company

***

N26 has today launched cryptocurrency trading

N26, the German neobank valued at $9 billion, has launched cryptocurrency trading tools via a partnership with investment platform Bitpanda.

Starting today, customers in Austria will be able to trade over 100 tokens, including dogecoin, SOL, AVAX and shiba inu, according to a statement on Thursday. These features will be rolled out to other markets in the coming months.

These tools are enabled through APIs from Bitpanda’s white-label business that allows platforms to tap into its trading tools. It will be available to access via the trading section of the N26 app’s forthcoming “Finances” tab.

“While cryptocurrencies have seen a decline in value over the last year, they remain a requested and interesting asset class for investors and a growing part of the financial system,” said N26 CEO Valentin Stalf in the announcement. “Cryptocurrency trading is often the entry point to investing for a new generation of investors who are looking to explore ways to grow their wealth.”

The Block reported in July last year that the German neobank was working with a “top-tier crypto exchange” on a new trading feature. This was initially pegged for a late 2021 release.

While N26 has over 8 million customers across Europe, many will have to wait to access the new features. Bitpanda is yet to obtain a license from Germany’s financial regulator, BaFin, meaning that the launch of N26 Crypto in its native country is currently not set in stone.

“The BaFin license comes with a particularly high priority,” said a Bitpanda spokesperson. “We have been in the process of acquiring the most extensive license for some time now in order to create a serious and regulated environment for investments in digital assets in Germany.”

Along with Austrian regulatory approval, Bitpanda is also registered with the French, Italian, Swedish and Spanish regulatory authorities — key markets for N26.

Source The Block

***

Fintech giant Plaid is releasing its first crypto-native product called “Wallet Onboard”

Marketed for developers, Plaid’s new crypto wallet interface will enable Web3 builders to easily access over 300 wallets, including MetaMask, Ledger, Coinbase Wallet, and Trust Wallet.

Plaid is most famous in traditional finance for Plaid Link — a banking Application Programming Interface (API) that acts as a client-side intermediary between a person’s bank accounts and their applications.

Wallet Onboard works in a similar way. Users who want to “connect wallet” to any blockchain-based application, be it a lender, exchange, game, or NFT marketplace, will see a drop-down screen from Plaid showing recently used wallets and offering to connect to their wallet of choice.

Plaid says this makes developers’ jobs easier since they currently have to build custom wallet connections to their own apps, increasing their development budget and potentially opening doors to security risks, like bugs or exploits.

Wallet Onboard can also host different kinds of wallets, including browser plugins, applications, and hardware wallets. To safeguard privacy, Wallet Onboard does not store wallet addresses.

Wallet Onboard currently only works with Ethereum and EVM-compatible chains, but Plaid may branch out and connect with Solana and other blockchains.

Trust is a big part of Plaid’s sales pitch for Wallet Onboard, according to the company’s head of identity Alain Meier, who says the new tool utilizes new identity verification features that were rolled out across Plaid services last week.

One such tool is the new autofill function, which verifies a user’s identity through phone number and date of birth; the other is behavioral analytics. Behavioral analytics can tell when a user’s device may be compromised by, for instance, measuring the time it takes for a user to fill in essential details in a form.

Plaid is also trying to create an identity verification protocol that won’t send data to an app. For instance, for age-restricted apps, Plaid could verify the account without sharing the user’s birth date.

Considering it’s barely three weeks into October and it has already been the biggest month in what has been the worst year of all time for crypto thefts, the industry can only hope that more traditional fintech companies like Plaid will contribute to keep the space secure from crime.

Source Decrypt

***

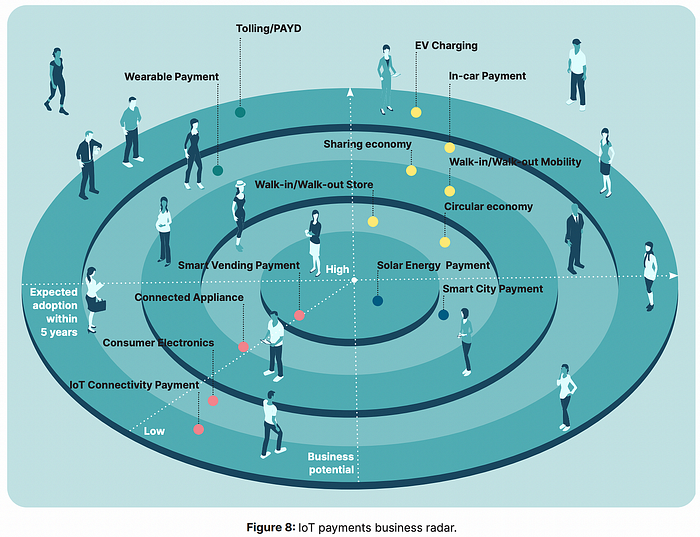

IoT payments will help accelerate the development of sharing economy platforms

There were over 38.5 billion connected devices in 202029 (triple the number in 2015). From this growth trajectory, billions of additional IoT payment transactions can be expected, yet most of these opportunities still remain untapped today. For example, a smart “personal shopper” could search for a specific product and close the deal automatically at the given permissible price on behalf of the consumer.

Solar panels could sell spare energy to other consumers/machines, with dynamic pricing and corresponding payment transactions being handled autonomously between two devices, enabled by blockchain technology. With so many potential use cases, it is important to identify which ones offer the greatest business opportunities for your organisation now and in the future. Figure 8 provides an assessment of the expected adoption and business potential for many IoT payments use cases. You may find it useful to prepare your own version of this radar for your company, taking into account factors like market traction (as assessed thorough interactions and discussions with your partners and your clients), market size, expected transaction volumes and expected customer adoption.

Source Worldline

***

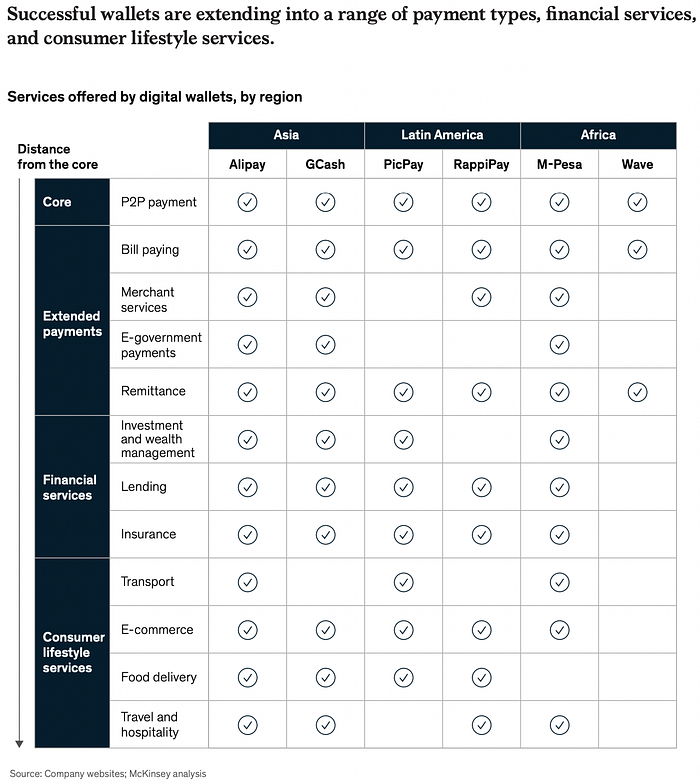

Wallets are exploring several monetization paths

To create profitable income streams, wallets are entering other payment arenas, such as bill payment, merchant services, and remittances. They are offering a more comprehensive range of financial services, including investment and wealth management, lending, and insurance. And they are providing lifestyle services, including transport, e-commerce, and food delivery to become a one-stop shop for consumers.

Extended payments.

In extended payments, wallets are offering a range of services, including merchant services such as universal payments acceptance, business digitization, loyalty programs, inventory management, and reconciliation. For example, MoMo offers merchants a set of tools to improve discoverability, access a voucher marketplace, and integrate loyalty programs.

Financial services.

Wallets’ offerings span several types of financial services:

— Investment and wealth management services include micro-investments for mass and upper mass markets, money-market funds, and linked high-interest bank accounts with easy onboarding.

— Lending can take place through partnerships or by using the wallet’s own balance sheet.

— Insurance offerings include travel, health, personal accident, and other forms of coverage.

As wallets extend their offerings into a wider range of payment solutions and financial services, some of them are transitioning into digital banks, a trend most advanced in Asia. Though becoming a bank subjects wallets to higher capital requirements and greater regulatory oversight, it also allows them to monetize their surplus balances and offer their customers a broad suite of lending products.

Consumer lifestyle services.

Wallets are also expanding into consumer lifestyle services in areas such as transport, e-commerce, entertainment, travel, and discount vouchers. In addition, they provide data services that enable mini-app providers to personalize their advertising. Being part of a super app gives these mini-app players access to an extensive customer base in return for a share of the revenues generated.

In the future, some emerging-market wallets may wish to take advantage of their payment rails and credit-scoring systems by offering a platformas-a-service solution, as global remittance player Wise has done with its Wise Platform.

Source McKinsey & Company

***

What makes super apps super?

Super apps. Elon Musk wants to build one and they’re already hugely popular in Asia.

So we all know what an app is, right? But what makes an app super?

11:FS’s David Barton-Grimley breaks down what super apps are, the popularity of them in Asia, how possible it is we may see a super app in the west and if we do, who is going to build it?

***

Successful implementation of hyper-personalization in banking

Successful implementation of hyper-personalization is about more than shiny new technology or an off -the-shelf approach. Leading banks have shown that the transformation needs to be founded on a strategic vision and willingness to make changes both to mindset and operations. These banks view their personalization ambitions through the lenses of their plans for the wider business. They also favor highly structured implementation based on fi ve key levers that create business impact in personalization; scale, variety, precision, velocity, and effi ciency.

The cornerstone of any implementation should be a vision of how hyper-personalization will function, and a deep understanding of how the tech and operating model will operate. The most advanced banks often build their offerings on five key building blocks. The first of these is based on the principle that there can be no effective change without organizational conviction. This means that banks need to cast off established orthodoxies, take a strategic approach to transformation, and be forensic on the drivers of change. The CRM needs to be placed at the center of the value creation process, and banks need agile, cross-functional teams to support the transition.

The second building block is about communication and action variants, deep behavioral analysis, and advanced orchestration, Data science teams need to both change the way predictive models are implemented and applied and take more responsibility for managing communications and their impacts. They need to step away from their screens and become storytellers around the benefits of change. Creative teams, meanwhile, need to massproduce and constantly refine content, while embedding AI/ML recommendations into the creative process and overcoming the urge to manually target the communicating — a tough ask for cohorts that are accustomed to being in control. However, only by putting AI/ML at the centre of communication targeting can they produce the acuity and responsiveness that will catalyze results. As a precondition of efficiency in the mass production of content, marketing and compliance functions need to be closely involved.

Pivotal to positive business outcomes is to start with the logic that needs to be embedded in the tech platform. Essential elements of this third building block include click and tap stream capturing, event detection, and real-time decisions for both online and offline channels. In the background, building blocks four and five are advanced data streaming capabilities and the ability to scale use cases in the cloud are essential.

Only once these five building blocks are in place or are at least thoroughly understood and designed, do leading banks go out into the market and start selecting the best fitting tech platform.

Source Boston Consulting Group (BCG)

***

India Fintech Report 2022: Sailing Through Turbulent Tides

India’s consumption story is back on track in 2022, driven by a favourable demographic dividend, increasing digitisation, improving public infrastructure, and continued technological innovation. As Covid-19 concerns recede and demand rebounds, the country’s population will resume its shift from an income pyramid to a diamond-shaped economy as lower-income households ascend to middle-income levels. Across income levels, consumption is expected to grow from $1.8–$1.9 trillion in FY21 to about $3 trillion by FY26 due to increased demand from an added 4 million affluent and 33 million mass affluent households. Along with households, micro, small, and medium enterprises (MSMEs) will be key to the economy, contributing an expected $1.3 trillion in gross value added by FY26.

Despite this expected growth, both household consumption and MSMEs remain underserved by formal credit. Credit penetration in most living expenditure categories is less than 5% for households. MSMEs also lack access to formal credit, with more than 60% relying on costly informal sources of credit. This funding gap is expected to provide strategic opportunities for fintechs.

Digital financial services (FS) are accelerating financial inclusion, democratising access, and spurring personalisation of products and customer journeys. With a strong foundation provided by the Jan Dhan-Aadhaar-Mobile (JAM) trinity, Unified Payments Interface (UPI) rails, and other positive regulatory frameworks, the pandemic has aided acceleration in digital adoption and provided a fillip to digital FS solutions by incumbents (banks, traditional NBFCs, insurers, etc.) and insurgents (fintechs). With expected growth in smartphone users to approximately 1.1 billion by FY26, up from about 750 million today, and more than 850 million Internet users in FY26, up from about 650 million today, India is shifting towards a mobile-first economy, especially in FS.

***

20 open banking use cases you should know about according to Yapily

1) Identity verification

Around €5.7 billion is lost during the onboarding process. Why? Because financial services still rely on physical documents for identity verification. The paradox is that paper documents are riskier than digital credentials. In fact, they’ve contributed to a surge in identity fraud. But with access to data, companies can…

Retrieve identity information in seconds

Validate a customer’s source of wealth

Pull data to support fraud analysis

2) Personal finance management

With every corner of the country feeling the effects of skyrocketing inflation, personal finance management has become a significant use case. Data aggregation enables companies to access and combine customer bank account data, providing tailored support with money management and actionable insights.

3) Payment reconciliation

Accessibility aside, spreadsheets weren’t made to hold a year’s worth of financial data. So, why do three million SMEs still use them? Open banking enables smart reconciliation by enabling businesses to see all of their transactions in one place.

4) Income verification

Whether it’s lending or renting, proof of income is at the core of a decision. It’s a lengthy process… particularly for those who are self-employed. In fact, business owners are twice as likely to be rejected for a mortgage. But with open banking, income verification is instant.

5) Affordability check

Affordability is key for lenders, whether it’s consumer or business lending. But, when only considering a small snapshot of a potential borrower’s financial position, it can be difficult to understand real affordability. Open banking enables lenders to analyse financial data for up to two years, providing a clear and accurate affordability profile.

6) Creditworthiness assessment

While affordability determines whether an applicant can afford to borrow, creditworthiness looks at how likely they are to pay it back. Credit scores are a fundamental deciding factor. But, those three-digit numbers disregard millions who are still improving their finances. Open banking allows lenders to access real-time insights, so they can make more informed decisions about who to lend to.

7) Account top-ups

We pay by card for most things. But, card payments aren’t all they’ve cracked up to be. Take account top-ups, for instance. Depositing by card can take hours to be approved. But with account-to-account payments, settlement is instant.

8) Invoice payments

Paper invoices haven’t gone anywhere, and they’re fuelling a late payment crisis among small businesses. Since invoices have always been paid by bank transfer, open banking payments are essentially an upgrade. The only difference is, they can be embedded into the checkout flow for a fast and frictionless experience.

and many more…

Source Yapily

***

Brex and Ramp rivalry

Corporate spend management has entered a period some analysts call “the great convergence.” Companies like Ramp, Brex, Mercury, and Airbase are increasingly moving toward offering all the same services, like charge cards, bill pay, and even B2B “buy now, pay later.” But as the market matures, leading companies Brex and Ramp are surrendering their dreams of owning the entire market — even though much of it has yet to be tamed — and moving toward more of a “divide and conquer” mentality.

Brex is still facing an identity crisis. When Brex controversially let its SMB customers go in June, Eric Glyman, the CEO of rival Ramp, told Protocol it was a “very, very good month” for his company.

- Brex co-founder Henrique Dubugras said during a talk at the TechCrunch Disrupt conference last week that trying to serve both SMBs and startups was the company’s “biggest mistake.”

- But his definition of SMBs feels shaky. Back in June, Dubugras told TechCrunch that Brex’s definition of SMBs was companies without “professional” funding. Yet at Disrupt, Dubugras seemed to contradict that, saying his company was totally down with “boot-strapped” startups too. Generously, you could say the common thread for Brex is serving companies with an accelerated growth strategy.

- Ramp, meanwhile, likes customers with money — slower-growing companies that are profitable earlier on. “I think in the startup world, people forget most businesses are profitable,” Glyman said. He argues that small and medium-sized businesses without a moonshot strategy are a strong, sustainable customer base.

Because they’re targeting different customers, their marketing is different. Brex is appealing to startup hype culture, and Ramp to an ethos of humble growth.

- Brex’s marketing feels straight out of the year the company was founded, 2017, when WeWork was hosting beer-soaked getaways for employees with Florence + the Machine performing. At LA Tech Week, Brex’s two buzziest events were a media-restricted yacht party and a mansion party serving Captain Morgan and Bombay shots, no chaser, at what was once the influencer-filled Hype House. At TechCrunch Disrupt, attendees were greeted by a giant floating

- “Brex” sign and a built-out coworking area immediately upon entering the expo floor.

- Brex touts customers like DoorDash and Coinbase: the kind of companies its startup clients hope one day to be.

- Glyman, meanwhile, described Ramp’s marketing persona as “nice but understated.” Much of the credit card industry’s marketing, historically, has been to play up the wonders of all the extravagant things you can charge on a card, like fancy flights. Glyman said he wants to do the opposite.

- “If you can help people go home earlier and spend time with their families and do more things for less, I think that should work,” he said. Ramp wasn’t even on the expo floor at Disrupt.

Source Protocol

***

Open decentralization: How to decentralize tokenization protocols

Tokenization protocols are another type of emerging web3 system. In these systems, assets are onboarded to a blockchain, tokenized by a smart contract protocol, and then sold or used for other purposes. Types of tokenization protocols include serial NFT-minting projects, digital asset marketplaces, and protocols that tokenize real-world assets.

The open decentralization model below reflects:

- assets brought on-chain from multiple providers through a shared smart contract protocol;

- the smart contract protocol tokenizing such assets;

the sale or use of such tokenized assets through multiple clients;

- native digital asset distributions and incentivization mechanisms; and

- the launching of DAO governance with respect to the community intellectual property and DAO treasury.

In this model, economic decentralization is achieved through sufficient diversity of inputs (asset providers) and outputs (asset acquirors), as well as the decentralization of the layers through which the tokenized assets flow (the blockchain, the smart contracts, and the clients).

The protocol’s DAO could also use explicit incentives (fungible token awards, no commissions/ fees, etc.) to:

- incentivize asset providers to provide assets to the system;

- incentivize clients to make a market in the tokenized assets; and

- incentivize acquirors to acquire such assets or to consume them.

While the initial developer company may initially play a significant part in any of these roles (asset provider, client operator, asset acquiror), once the system is decentralized, the developer company would eventually be just one of many actors in any given role. This would limit the risk of any significant information asymmetries accruing to it and reduce the reliance on its managerial efforts. In addition, many roles could be undertaken by the DAO and/ or subDAOs.

Over time, the explicit incentives could also be adjusted to account for potential shortfalls on either the supply side or the demand side. In a decentralized marketplace for instance, token incentives to sellers (the supply side) could be increased to bring more goods for sale onto the platform; and token incentives to buyers (the demand side) could be increased to encourage more purchases.

From a legal decentralization perspective, the key questions, yet again, would be: Are the essential managerial efforts of any third party necessary to drive the success or failure of the web3 system? And would there be the potential for significant information asymmetries to arise? The answer to both questions depends on whether the DAO could effectively manage its incentives to balance supply and demand as in the example above — but more broadly, it’s really about preventing any single asset provider, asset acquiror, or client from becoming so important that the success of the entire system relies on any one entity’s efforts.

Source Andreessen Horowitz